The impact of Chinese-manufactured EVs on Europe's primary markets

Although SAIC's MG brand has made a noteworthy impression, the majority of Chinese EVs making their way into Europe belong to established brands like Tesla, Dacia, and Smart.

During the initial eight months, the MG4 secured the ninth position among top sellers in the compact segment. Additionally, it claimed the second spot for best-selling full-electric model within the segment, following the VW ID3.

In the initial seven months of this year, recent data reveals that one out of every five battery-electric vehicles registered in Western Europe were imported from China, with Tesla taking the lead.

The surge in Chinese-manufactured vehicles making their way to the region has been closely monitored. Just last month, Ursula von der Leyen, President of the European Commission, declared an inquiry into the influence of the Chinese government in reducing the prices of cars manufactured in China and sold in Europe, particularly electric vehicles.

Von der Leyen commented "Their prices are being artificially suppressed by substantial government subsidies. This is causing distortions in our market."

Of the 224,254 EVs imported from China and registered in Western Europe, 136,823 were from Western automakers, of which Tesla, which makes cars in Shanghai (shown), accounted for 68 percent, data from Schmidt Automotive Research shows.

Out of the 224,254 electric vehicles brought in from China and registered in Western Europe, those originating from Western automakers numbered 136,823. Among these, Tesla held the majority share at 68 percent, equivalent to 93,700 EVs, based on data from Schmidt Automotive Research. It's worth noting that Western Europe represents the predominant market for electric vehicle sales in the region.

The American electric vehicle manufacturer transports Model 3s from its Shanghai facility to Europe, along with right-hand-drive Model Ys destined for the U.K. Model Ys for continental Europe are produced at Tesla's plant near Berlin.

Tesla, alongside European automakers like Renault and BMW that import vehicles from China, are included in the ongoing subsidy investigation, as reported by the Financial Times.

Thanks to SAIC-owned MG's leadership, Chinese brands, including Polestar, contributed to a total of 87,431 sales of fully electric vehicles. This secured them an 8.2 percent share of the overall electric vehicle market in Western Europe for the first seven months, according to data from Schmidt.

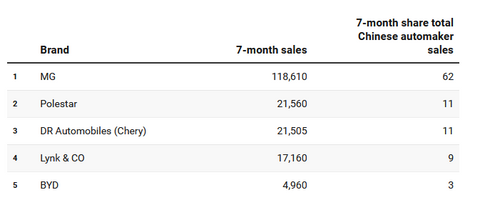

The leaders

Top-selling Chinese brands in Western Europe (all fuel types)

For a considerable period, European automakers have expressed apprehensions about China's highly efficient supply chain, particularly in terms of battery materials. They fear that even with a 10 percent tariff in place, Chinese brands could maintain a significant cost advantage in the European market.

Stellantis CEO Carlos Tavares, speaking at the 2022 Paris auto show, emphasized "The European market is wide open to the Chinese, and we do not know if their strategy is to grab market share at a loss and increase their price later."

The Chinese automotive presence in Europe has been rapidly expanding, with their market share climbing from 2.0 percent in 2020 to 2.8 percent in the first seven months of the current year, up from a mere 0.1 percent in 2019.

Notably, MG, in particular, is making significant strides in crucial market segments.

According to figures from market researcher Dataforce, the MG4 secured the ninth position in terms of sales in the compact segment during the first eight months, with a volume of 43,045. Moreover, it emerged as the second-best selling full-electric model in the segment, trailing only the Volkswagen ID3.

China's BYD, which is led by the Atto 3 (shown), was Sweden's top-selling brand in July.

The MG ZS, available in both combustion engine and full-electric versions, secured the 13th position among best-selling small SUVs in Europe, with a total of 49,656 registrations. Among full-electric models in this segment, it ranked fourth.

MG's most significant impact has been felt in the U.K., where it stands as the 11th best-selling brand after eight months, according to data from the automotive advocacy group SMMT.

In the European region, the U.K. stands out as China's largest export market, with 118,000 units shipped in the initial seven months, as reported by the China Association of Automobile Manufacturers.

Spain follows as the second-largest export market for Chinese vehicles during the same period, accounting for 84,000 units.

Sweden demonstrated the highest percentage share of Chinese car sales between January and July, comprising 5.6 percent of total sales, according to Schmidt's data.

During the month of July, BYD from China claimed the top spot in terms of overall brand sales in the country. Schmidt Automotive Research's Matthias Schmidt noted that July is typically one of the slower months for car sales in the calendar year.

Among European countries, the U.K. recorded the second-largest share of sales from Chinese automakers during this period, accounting for 5.0 percent, followed closely by the Netherlands with 4.6 percent (see table below).

Northern focus

Top five European markets for Chinese vehicles based on market share

Apart from MG, the influence of Chinese automakers on established players remains relatively modest.

MG commanded the lion's share at 62 percent of all Chinese car sales in the initial seven months, while Polestar and DR Automobiles (which rebrands cars produced by China's Chery Automobile) each held an 11 percent share. BYD accounted for a mere 2.6 percent, according to data from Schmidt.

As of now, the cost advantage that allows Chinese domestic brands to sell their electric vehicles domestically at nearly half the price of equivalent models in Europe hasn't resulted in a substantial influx of budget models in the region.

All Chinese vehicles sold in Europe incur significant additional expenses for importation. A recent report from the investment bank UBS evaluated the production cost of the new BYD Seal midsize electric sedan and estimated that the Chinese price of 26,572 euros increased to 35,342 euros once imported.

This total included shipping costs of 2,000 euros, a 10 percent import tariff of 3,040 euros, sales distribution expenses of 1,500 euros, and the variance in value-added tax of 2,230 euros.

BYD in Europe has been reluctant to sell on value alone, focusing on the higher-range Seal EV with an 82.2-kilowatt-hour battery. That car sells for the equivalent of 28,800 euros in China, but costs 45,695 pounds (52,800 euros) in the U.K., one of the first European markets for which BYD has announced pricing for the car.

UBS determined that BYD can manufacture the Seal in China for 35 percent less than a VW ID3 made in Germany, after conducting an in-depth analysis of the model.

The bank remained unconvinced that state assistance played a significant role in this cost advantage. Patrick Hummel, UBS analyst, noted, "It's quite possible … that price competitiveness is to a great extent actual competitiveness rather than the effect of subsidies," in response to the European inquiry into the impact of subsidies.

The strong-selling Dacia Spring EV is built in China.

Despite the added expenses associated with importing models from China, numerous European and Japanese automakers have already begun shipping vehicles from China to Europe.

Current examples include the BMW iX3, a midsize electric SUV, the Dacia Spring, a small EV, Citroen C5X, a midsize vehicle, and Tesla's Model 3 and Model Y. Honda is also shipping a range of models, including the e:Ny1, a small electric SUV, the CR-V, a midsize SUV, and the ZR-V, a compact SUV. Additionally, Smart's #1 and DS 9, a midsize car, are part of this list.

Looking ahead to the next year, VW Group's Cupra brand plans to import the Tavascan, a midsize electric SUV, from China. Meanwhile, BMW's Mini division will introduce the Cooper, a small EV, and the Aceman, a small SUV. Volvo will import the EX30, a small electric SUV, and Smart will bring the #3 to Europe.

The European market has proven to be challenging for many new Chinese brands.

In the first eight months of 2023, several brands, including Hongqi, Xpeng, Aiways, LEVC (Geely's taxi brand), Dongfeng Sokon Automobile, and SAIC's Maxus, saw a decline in sales, as reported by Dataforce. In contrast, the overall car market in the same period experienced an 18 percent growth.

On a more positive note, other Chinese brands have shown considerable promise. Nio, for instance, exhibited an impressive 109 percent increase with 1,475 sales. Great Wall's Ora brand achieved 3,551 sales in this period. BYD experienced a substantial surge of 470 percent, totaling 7,729 sales. Geely's Lynk & CO also demonstrated significant growth, reaching 19,664 sales, marking a 50 percent increase from the previous year.

Polestar's growth amounted to 62 percent with 25,122 sales, while MG retained its leadership position with 137,718 sales, reflecting a remarkable 135 percent increase.

In reality, the threat posed by Chinese automakers, with the exception of MG, appears to be more formidable in theory than in actual practice.

---------This article is partly excerpted from Reuters.